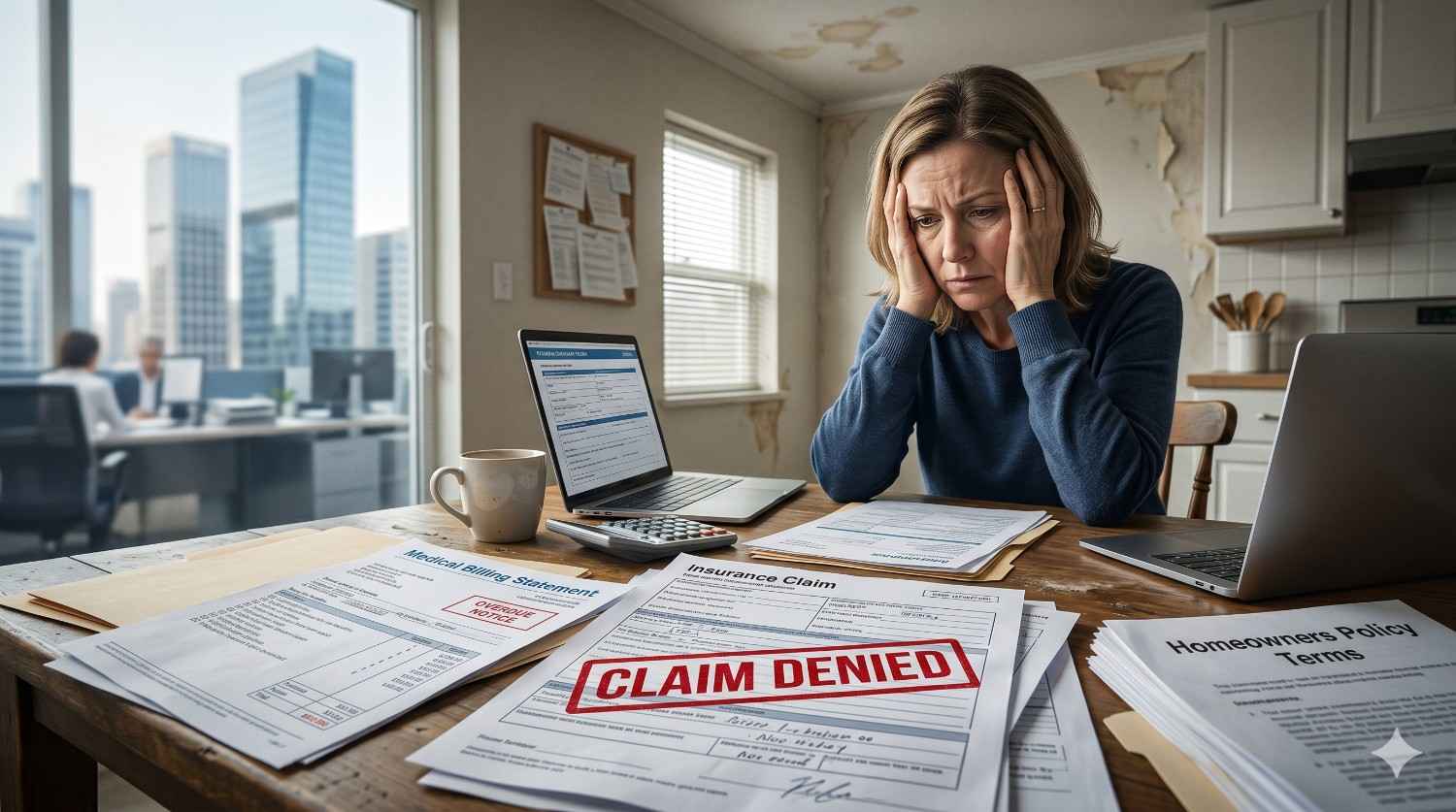

Allstate consistently ranks as the insurance company that denies the most claims in the United States, particularly for homeowners and property-related coverage. Independent investigations and consumer reports have repeatedly flagged Allstate for high denial rates, delayed payouts, and disputed settlements. For homeowners, landlords, and property managers, understanding which insurers carry these patterns helps protect property investments and ensures repairs and damage claims move forward without costly setbacks.

The Insurance Company With the Highest Claim Denial Rates

Allstate is widely reported as the insurance company that denies the most claims in the U.S., based on multi-year investigations into homeowner and auto claim handling. Independent watchdog reports have cited internal practices that delay, deny, or defend payouts, especially on property damage cases involving roofing, water damage, and structural repairs.

How Denial Rates Are Measured

Denial rates are tracked through state department of insurance complaint ratios, consumer advocacy investigations, and class-action filings. The National Association of Insurance Commissioners publishes annual complaint indexes that compare insurers against industry averages. Insurers with consistently elevated complaint ratios for claim handling, denial frequency, and delay patterns appear at the top of denial-related rankings year after year.

Why Some Insurers Deny More Claims Than Others

Insurers with the highest denial rates often share three traits: aggressive cost-containment policies, narrow policy interpretation, and reliance on third-party adjusters who minimize damage estimates. Property claims involving roof damage, water intrusion, or wear-and-tear disputes are denied most frequently because insurers categorize them as maintenance issues rather than covered perils.

Understanding which insurers deny claims most often is only half the answer. The deeper concern is how denials affect property owners directly, and how proper water damage documentation can change the outcome of a disputed claim.

What This Means for Homeowners and Property Managers

For homeowners, landlords, and property managers, a denied claim can mean thousands in out-of-pocket repair costs and delayed property restoration. Denials often hit hardest on roofing, plumbing leaks, mold remediation, and storm damage. Property managers handling multiple units face compounding losses when claims across properties get systematically reduced or refused. The financial impact extends beyond repairs, affecting tenant safety, property value, and insurance renewal terms.

Common Reasons Property Claims Get Denied

Most property claim denials trace back to four causes: insufficient documentation, missed deadlines, policy exclusions, and pre-existing damage disputes. Insurers frequently argue that damage existed before the policy period or resulted from neglect. Scheduling a professional roof inspection before filing creates documented evidence that strengthens the claim and counters denial tactics.

How to Reduce the Risk of a Denied Claim

Reducing denial risk starts with prevention and documentation. Photograph property conditions annually, keep receipts for repairs, and review policy exclusions before storm season. File claims within required deadlines and request written explanations for any denial. Consistent routine property maintenance directly addresses the neglect argument insurers use to refuse coverage, keeping properties claim-ready year-round.

Working with licensed service professionals who provide detailed invoices and condition reports adds another layer of protection. These records become critical evidence if a claim is challenged.

Conclusion

Allstate leads U.S. insurers in claim denial frequency, particularly for property-related damage involving roofing, water, and structural repairs. Knowing this helps homeowners and property managers prepare smarter.

For landlords and property managers, the right documentation, inspections, and maintenance routines turn denied claims into approved ones, protecting long-term property value.

We help you stay ahead with trusted inspections, repairs, and maintenance. Contact Mr. Local Services today to keep your property claim-ready.

Frequently Asked Questions

Which insurance company has the highest complaint ratio?

Allstate and State Farm have historically posted elevated complaint ratios with state insurance departments, particularly for delayed and denied property damage claims.

What is the most common reason a homeowners claim is denied?

Insufficient documentation and pre-existing damage disputes are the top reasons. Insurers often argue damage resulted from neglect rather than a covered event.

Can I dispute a denied insurance claim?

Yes. Request a written denial explanation, gather inspection reports and photos, and file an appeal. State insurance departments accept formal complaints against insurers.

Does filing a claim raise my insurance premium?

Often yes. Even denied claims can appear on your CLUE report and influence renewal pricing, especially for repeated property damage filings.

How long do insurers have to respond to a claim?

Most states require insurers to acknowledge claims within 15 days and issue a decision within 30 to 60 days, depending on local regulations.