Yes, homeowners insurance typically pays for water damage, but only when the damage is sudden and accidental. Coverage depends heavily on the cause, the policy type, and how quickly the issue is reported. Gradual leaks, flood damage, and neglected maintenance are usually excluded. Understanding the difference between covered and uncovered scenarios helps homeowners, landlords, and property managers avoid claim denials and protect their property investment when unexpected water damage strikes.

Does Homeowners Insurance Cover Water Damage?

Standard homeowners insurance covers sudden and accidental water damage, such as a burst pipe, an overflowing washing machine, or a roof leak from a storm. It does not cover flood damage, gradual leaks, or damage caused by poor maintenance. Flood coverage requires a separate policy through the National Flood Insurance Program.

What Types of Water Damage Are Covered

Most policies cover internal water damage that happens unexpectedly. This includes burst pipes from freezing temperatures, accidental overflow from appliances like dishwashers and water heaters, sudden plumbing failures, and water damage from extinguishing a fire. Storm-related damage, such as wind-driven rain entering through a damaged roof, is usually covered. Water damage from a sudden HVAC malfunction or a ruptured supply line also falls within standard coverage when the event was not preventable.

What Types of Water Damage Are Not Covered

Insurance excludes damage from flooding caused by external water sources, including overflowing rivers, heavy rainfall pooling around foundations, and storm surges. Gradual leaks, mold from long-term moisture, sewer backups, and damage from unrepaired issues are also excluded. Most importantly, policies deny claims tied to neglected maintenance. If a slow roof leak or dripping pipe goes unaddressed for months, insurers consider the resulting damage preventable and refuse coverage.

Understanding what your policy covers is only half the equation. The faster water damage is addressed, the stronger the claim. Professional water damage restoration often determines whether an insurer approves or disputes a payout.

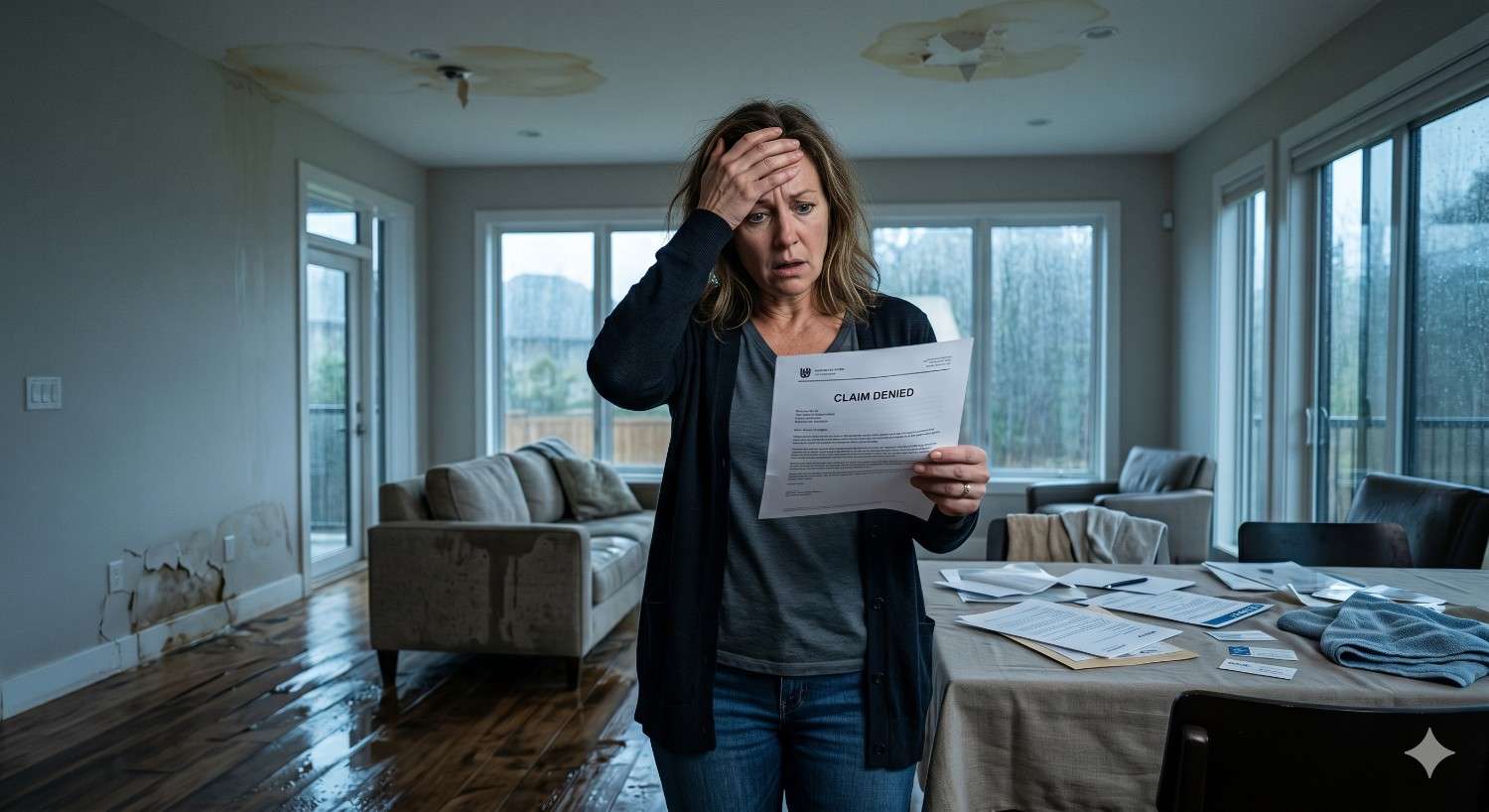

When Water Damage Claims Get Denied

Claim denials usually come down to one issue: the insurer believes the damage was preventable. Adjusters look closely at the timeline, the source, and the property’s maintenance history. If evidence suggests the homeowner ignored warning signs, the claim is at risk.

Gradual Leaks, Neglect, and Maintenance Issues

Slow leaks behind walls, deteriorating caulking, aging water heaters, and damaged shingles are the most common denial triggers. Insurers expect homeowners to perform regular upkeep, including timely roof leak repairs, plumbing inspections, and appliance maintenance. Documentation matters. Keeping receipts, inspection reports, and dated photos of repairs strengthens your position. If an adjuster argues the damage developed over time, proof of consistent maintenance becomes the strongest defense against denial.

How to File a Water Damage Insurance Claim

Act quickly. Stop the water source, document everything with photos and video, and contact your insurer within 24 to 48 hours. Make temporary repairs to prevent further damage, but keep all receipts. Avoid discarding damaged items until the adjuster inspects them. Provide a detailed inventory of losses with estimated values.

Most insurers send an adjuster within a few days. Hire licensed restoration professionals for cleanup, and request itemized invoices. Early plumbing leak detection before damage spreads can also reduce out-of-pocket costs and improve claim outcomes significantly.

Conclusion

Homeowners insurance pays for water damage when it is sudden, accidental, and properly documented. Coverage hinges on the cause, the timeline, and maintenance history.

For landlords, homeowners, and property managers, prevention and quick response remain the most reliable protections against costly claim denials and long-term property loss.

Need fast, dependable help with water damage, repairs, or maintenance? Mr. Local Services connects you with trusted professionals nationwide. Get started today.

Frequently Asked Questions

Does homeowners insurance cover burst pipes?

Yes. Burst pipes are considered sudden and accidental, so most standard policies cover the resulting water damage and pipe repair, minus your deductible.

Will insurance pay for water damage from a leaking roof?

Coverage depends on the cause. Storm-related roof leaks are typically covered, while leaks from worn shingles or unaddressed maintenance issues are usually denied.

Is mold from water damage covered by insurance?

Mold is covered only when it results from a covered water event. Mold from gradual leaks, humidity, or neglect is almost always excluded.

How long do I have to file a water damage claim?

Most insurers require notification within 24 to 72 hours. Filing quickly preserves evidence, prevents further damage, and strengthens your overall claim approval odds.

Does homeowners insurance cover flood damage?

No. Flood damage from external sources requires a separate flood insurance policy, typically purchased through the National Flood Insurance Program or private insurers.